We are following up on our previous blogs about US residents with British pension schemes and our consideration of USA tax on QROPS . The fact is that a product has been used in the USA within pensions ( and standalone investments ) that probably should not have been. We refer to the sale of insurance bonds in the US!

We consider the debacle of insurance bonds in the US in this blog.

Reasons for the use of insurance bonds

We have cited many reasons where insurance bonds are useful tax planning tools for the well-off. However, we have also said that an insurance bond is not suitable for pension funds as a method of holding investments and certainly not suitable in some countries.

Insurance bonds in the US and British pensions

Insurance bonds are non-income producing assets and, as such, are hardly suitable for a pension that provides an income in retirement. Natural income (such as dividend and interest) cannot be taken if that is deemed a suitable income strategy, the retiree will always have to encash capital to get an income.

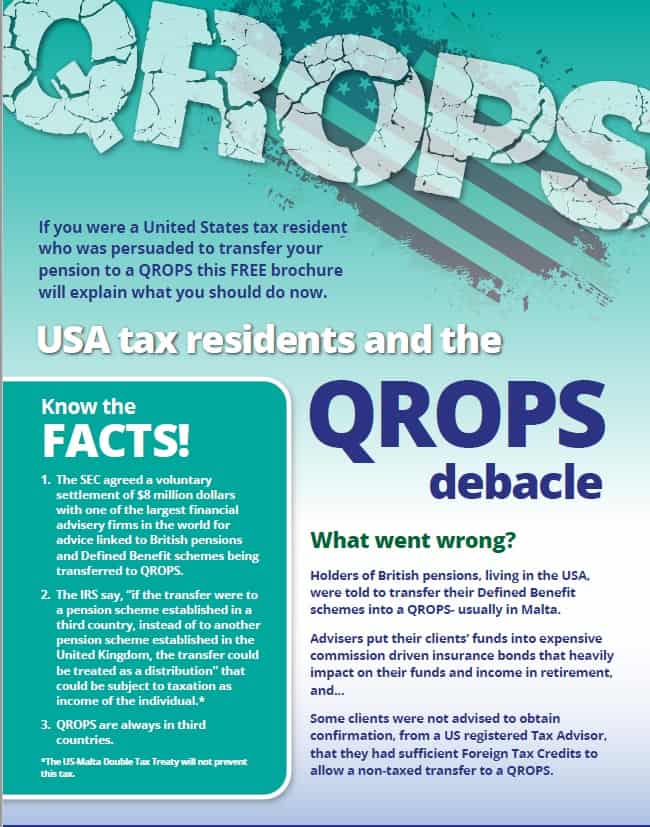

The problem as demonstrated in our first blog, for US residents with British pension schemes, is that people may have been deceived into paying high charges, and may not be fully aware of the tax implications of the transfer. When asked to review a case 2 years ago, we realised there was an imminent insurance bond debacle developing in the USA. Not only had the client not been told about the cost of the insurance bond, and the funds recommended within, but he had not understood the likely loss of growth of the fund and the reduced income in retirement.

Members of OpesFidelio, and EU network have been provided with a comprehensive spreadsheet that allows advisers to look at the potential costs and impact of cost savings of a platform vs an insurance bond. We hold an SEC licence for the US and are able to advise US residents.

Insurance Bond- Commission

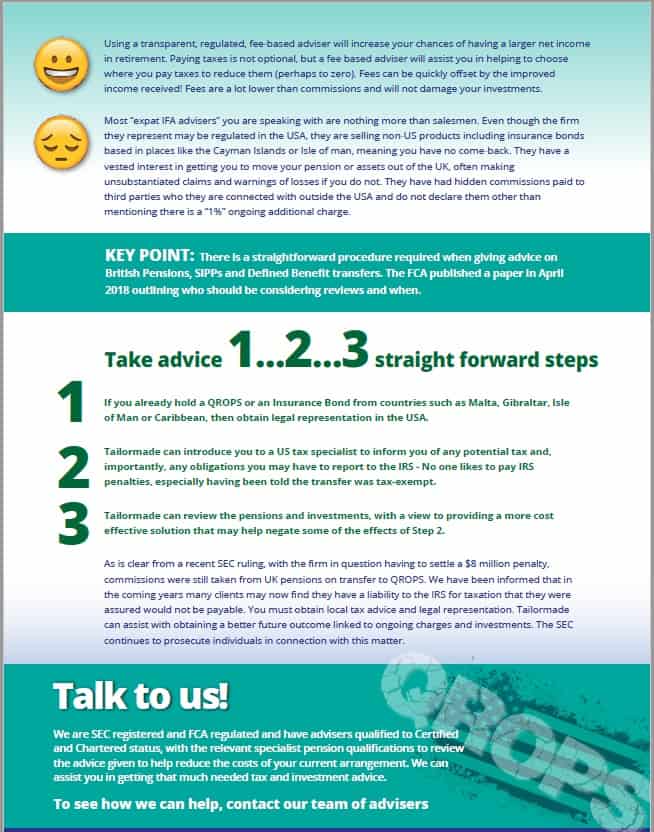

Let’s cut to the chase here, the reason insurance bonds in the US are sold (especially in pensions), is to generate substantial commissions. In nearly all cases these commissions are not disclosed, but they are sold as transparent products with a total cost of 1% pa – However, the real costs, with all the investments, is likely to be anything from 3.5% to 5% pa with a servicing charge and that puts an intolerable strain on your pensions and will reduce your income in retirement significantly.

Evidence of the true costs are now coming out, much later, as this shows

Commission like this is a clear conflict of interest and locks investors into an expensive insurance bond for between 5 to 10 years, where surrender penalties are applied upon access in may cases.

QROPS – What should I do if I have an insurance bond in the US?

If you have been advised to transfer to a QROPS, while US resident, then you really need to review the tax advice and the insurance bond within it.

We can provide access to US tax specialists to review the tax implications of the transfer, they can provide tax advice advice going forward and we can provide a Forensics Review of your insurance bond and investments.

It’s too late to stop the Insurance Bond Debacle in the USA but we can try and help those affected and we have a PDF that provides more detail.

Insurance Bond Debacle in the USA – Summary

There is no doubt that the recent SEC action will have raised a red flag over the advice that many have taken and no one knows the consequences for those that have transferred to QROPS, while US resident , both in terms of tax liabilities and lower returns from expensive products with high and undisclosed commissions.

Our contention is that it is better to take action to review those QROPS as soon as possible to limit any potential losses or problems in the future.

If you take no action then you will continue to incur losses. You are losing out by doing nothing!

For further information, please look at our brochure here-

The views expressed in this article are not to be construed as personal advice. You should contact a qualified and ideally regulated adviser in order to obtain up to date personal advice with regard to your own personal circumstances. If you do not then you are acting under your own authority and deemed “execution only”. The author does not except any liability for people acting without personalised advice, who base a decision on views expressed in this generic article. Where this article is dated then it is based on legislation as of the date. Legislation changes but articles are rarely updated, although sometimes a new article is written; so, please check for later articles or changes in legislation on official government websites, as this article should not be relied on in isolation.

This article was published on 11th July 2018

Related Stories:

- USA Tax On QROPS | Pension Legislation

- Spain- Insurance bonds in pensions, is there a tax advantage?

- Making a Goulash of Your Retirement ( Insurance bond and income )

- Offshore Bonds and SIPPs

- QROPS in Spain

Share this story